Tag: disney

-

Star on Disney+ is a Shallow Offering

This week Disney began its global rollout of ‘Star’ as part of its Disney+ service. In the US, Disney has a family of packages including Hulu and ESPN+, offering a package deal for all of them. But the rights situation is complicated. Although Hulu is basically owned by Disney now, it was originally a joint…

-

The Pricing of Apple TV+

Apple has announced that it’s upcoming TV service will cost £4.99 in the UK (and $4.99 in the US). That’s instantly brought a lot of comparisons with other services’ prices since it undercuts all of its major competitors. They will also give you a year free when you buy a new Apple device. However, I…

-

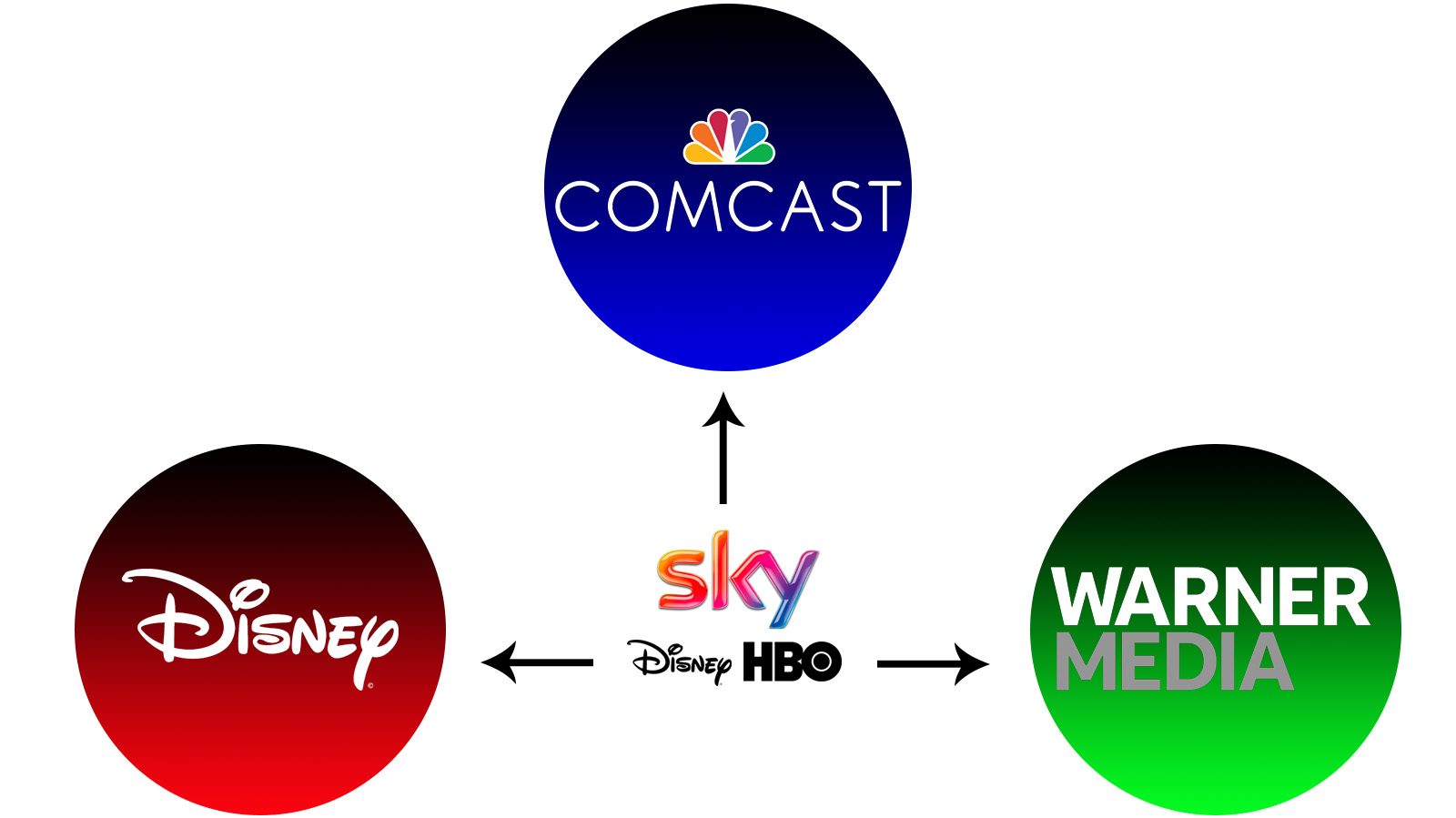

What Do Disney+ and HBO Max Mean for Sky?

Disney+ and Sky Earlier this year, we finally got some detail on Disney’s upcoming new service, Disney+. The new streaming service will launch on November 12 this year in the US at a monthly cost of $6.99 – discounted a little to $69.99 if you pay for a year up front. Or you can pay…

-

Netflix, Independent Cinema, and Hollywood’s New Business Model

The other day The Ringer published a piece about Netflix and their original movie strategy. The piece, entitled Netflix and Shrill listed the original movies that Netflix has already released in 2018 and challenged readers to see how many they recognised. For most people, the most familiar title will have been The Cloverfield Paradox. This…

-

Netflix and Disney

Last week came news that Disney would be pulling its movies from Netflix at the end of the current arrangement, and that Disney would in future launch its own streaming service. This licensing agreement generated a vast amount of coverage, much of it ill-informed, and ignoring wider issues in the market. There are a few…

-

Captain Phillips and Saving Mr Banks

Tom Hanks managed to somehow both open and close this year’s London Film Festival with a pair of very different films that I managed to see within twenty four hours of each other. Some film-makers demand to be seen, whatever they do. And Paul Greengrass is one such film-maker. Captain Phillips opened this year’s London…