Once again, this post is brought to you in association with RALF from DP Software and Services. I’ve used RALF for the past 9 years, and it’s my favourite RAJAR analysis tool. So I continue to be delighted to be able to bring you this analysis in association with them. For more details on RALF, contact Deryck Pritchard via this link or phone 07545 425677.

All views here are clearly my own!

Early August means the results of RAJAR Q2 2016, and most of the new second national DAB multiplex (D2) services are reporting for the first time.

The first thing to note is that overall listening is at its highest ever for radio. 48.687m people listening to the radio each week. While listening hours aren’t at a similarly high record level, the average radio listener listens for a solid 21.5 hours a week.

You can perhaps partially attribute this record to that launch of those new commercial services, which in the main have a cumulative effect on radio listening. And commercial reach has overtaken the BBC’s again, with 35.570m people listen to commercial radio each week – another all time high.

(It’s fair to add at this point that RAJAR updates its estimate of the UK population in Q2 each year, so if radio listening remains constant, then you would expect numbers to increase proportionately with the population regardless. But we do know that there are some real challenges at the younger end of the age spectrum for radio, so this remains a good result.)

New Services and National

This quarter saw the launch of no fewer than six completely new services on D2, as well as the movement across from D1 or up from local multiplexes, of a number of other services.

But I must confess that I’m interested in a couple of specific stations in particular. First off, Virgin Radio reports for the first time. It has delivered a reach of 409,000 with 1,453,000 listening hours – a result that seemed to be good enough to send everyone off to the pub on Wednesday afternoon!

Tim @cocker has been left in charge of Virgin Radio whilst everyone else is at the pub…

So for next 30 mins we want your requests please!

— Virgin Radio UK (@VirginRadioUK) August 3, 2016

Now the key thing here is any possible misattribution.

Recall that I previously looked after ratings for Virgin Radio as it changed to Absolute Radio back in September 2008. We were acutely aware that no matter how big our marketing budget (and it was never going to big enough), many listeners would continue to think of the station as Virgin Radio. If they were long term listeners, they might have been listening for 15 years at that point. And the station adopted a more adult approach of rebranding, slowly morphing from Virgin to Absolute, rather than the more usual ‘off air on Friday, back on air with new format on Monday’ approach that more regularly happens. The majority of the presenters remained the same, and the music was only very slightly tweaked – probably not enough that the average listener would notice. So the big job was to expunge the old name and get people calling the station by its new one.

As far as RAJAR went, we had a label in diaries that said something like “Absolute Radio (was Virgin Radio)” which is pretty typical, and helps respondents navigate the name change. Capital Liverpool still refers to Juice on its label, for example.

Of course the station initially took a massive hit in listening figures, and that label referencing Virgin Radio remained in RAJAR diaries for many subsequent quarters – indeed years. It takes a long time for people to forget a station’s name.

And now we get the new Virgin Radio, with the same logo, but nearly all new presenters. The music mix isn’t the same as Absolute Radio, although the new Virgin shares just under a third of its playlist (at time of writing) with Absolute.

So take that into account when you’re considering its figures. Looking at its figures in comparison with the other new launches from the Wireless Group (or should that be News Corp now?), this feels a little high for the first set of numbers. But then Absolute Radio has gone up this quarter too very slightly (see below), so maybe all is fine. One to watch…

What about the other new launches? TalkSport 2 saw a reach of 285,000 and 913,000 hours. As expected, they’ve picked up Absolute Radio’s second pick of Saturday afternoon Premier League football commentaries, so this may take time to grow as they build out their portfolio of sports.

TalkRadio is at 224,000 reach and 840,000 hours. That’s going to need to grow since speech radio isn’t cheap. I suspect that the success of this will be down to marketing. Fortunately for all of their stations, having a new owner who owns a series of national newspapers (and has interests via a parent company in a satellite TV network), marketing might prove to be a bit more achievable in the medium term.

In any case, these are decent results, and all have plenty of room to grow.

Mellow Magic achieved a respectable 380,000 audience, with nearly 1.6m listening hours, while Magic Chilled (which is DAB+ recall, so not available on all DAB radios even within the D2 transmission area) reached 233,000 listeners for 601,000 hours. I suspect Bauer will be perfectly happy with both as something to build on, and something to add into a Magic Network national sales proposition.

As an aside, Magic has also been running a series of pop-up DAB stations. We’ve had Magic Abba, and right now there’s Magic Soul Summer. Sadly, these don’t get measured by RAJAR as they’re on-air too briefly.

The final completely new service on D2 is Awesome Radio, but I don’t believe that it is currently being measured by RAJAR.

Elsewhere, there’s no doubt that Radio 1 has had another shocker, down 4.6% on the quarter and 9.4% on the year in reach terms. 9,455,000 is its lowest reach since 2003, and there are no immediate signs of improvement. Listening is actually up a little on the quarter, but also down on the year. As I’ve repeatedly mentioned previously, I believe this to be a larger problem than Radio 1 and more “radio” – although arguably Kiss is bucking the trend (see below).

Radio 2 is down a little, but nothing to be concerned about, with 15.3m listeners and “only” 179,000,000 hours, or 17% of all radio listening!

Radio 3 has had its best reach figures since 2011 at 2.2m, all the more surprising for not happening in a Proms period (they’ve just started). Hours are down a bit though. Meanwhile over at Classic FM, they’ve bounced back from last quarter’s very poor results, up 7.6% in reach to 5.5m. Cue lots of headlines about a classical music resurgence, which I don’t believe is true.

Radio 4 has had its best ever reach under the current methodology (i.e. since at least 1999), with just over 11.5m listeners. Can we put this squarely down to coverage of Brexit? Perhaps we can. Hours are also up, if not quite at record-breaking levels.

5Live also saw gains in the period – albeit, more modest – up 1.5% in reach to 5.858m reach.

Absolute Radio was fractionally up with a reach of 2.185m listeners this quarter, although listening was down. It’ll be worth watching closely with regard to any issues over misattribution as I mentioned above.

Talksport also had a good quarter, jumping 6.5% in reach and 15.4% in hours on the previous quarter. Perhaps it was helped by the a decent end of the season story and notably Leicester City? (Although arguably that should have also affected 5Live.)

Digital

Last quarter, you may recall, RAJAR reallocated listening to platforms for those who failed to record it properly. This led to something of a “bump” for digital listening. It rose to 44.1%.

So this quarter, it was going to be interesting to see if that one-time increase would slow growth. Q1 was also the quarter that new Christmas DAB sets tended to inflate numbers a little.

Well it turns out that it hasn’t dampened growth, and we’ve seen listening increase again to 45.3% of all listening hours now being on a digital platform. What’s more, of those who listen to the radio, 78.6% now choose to listen for at least some of their listening time via a digital platform.

Needless to say, these are both all-time highs.

Breaking that 45.3% down, 32.2% of listening is via a DAB radio (a record), while 8.0% is via the internet (also a record). Only DTV is fairly settled at 5.1%.

Streaming grows as broadband improves, smartphones become more normal, and data plans increase. In another year or so, we might be at one in ten hours of radio being streamed in the UK.

I was disappointed, but not at all surprised to see that Absolute 80s has registered a fall this quarter. Recall that this was the largest commercial digital only station. Last quarter Bauer moved it from the D1 to D2 multiplex. Unfortunately, there is significantly less coverage for D2, and stations like Absolute that moved across, saw decreases in availability. Maybe it was due a dip anyway, but it exhibited an 8.1% fall in reach and 9.9% fall in hours on the previous quarter.

Not everyone can switch to streamed listening or the digital television when they lose their DAB signal.

6 Music has another record reach, up fractionally on last quarter’s record reach to nearly 2.3m listeners listening for nearly 22m hours.

Radio 4 Extra seems to have rebounded a little from last quarter’s disappointing results, back to nearly 2m listeners.

Asian Network achieved an all-time record reach of 676,000 which will please them.

The BBC World Service was basically flat in reach (-0.8% on the quarter) at 1.454m, but down 5.5% in hours.

Finally, LBC is worth examining. Reach and hours across the network are at record highs under the current methodology. It’s reach is now 1.729m, up a massive 12.3% this quarter, and 16.7% on the year, while hours are even better with 17.5m up 15% on the quarter and 20% on the year. I think we can squarely put that gain down to Brexit, and indeed the question is whether they can hang onto that listening in future quarters. A really excellent performance.

Networks

The Kiss Network is an interesting one to keep an eye on. It seems to be continuing to grow, building out Kisstory and Kiss Fresh. And what’s interesting is that all the Kiss brands are young, with Kiss aged averaging 30, Kisstory 32, and Kiss Fresh 27. Radio 1 on the other hand averages 35. The Kiss Network has achieved a record 5.5m reach, up 5.4% on last quarter. And Kisstory is now only just behind Absolute 80s in the battle for best performing commercial digital station. Kiss and Kisstory also achieved record results in London.

The Capital Network is also growing, although we need to be careful because they’ve grown their portfolio of stations too. This quarter, the network is up 3.9% in hours to nearly 7.9m listeners, while hours have also grown very solidly by 7.4%.

The Heart Network isn’t doing quite as well, falling slightly this quarter in reach and hours. Nothing disastrous, but it doesn’t feel that Heart Extra has had any effect so far. But there is a curiosity here. Heart Extra is a service I can listen to on DAB, but it doesn’t arrive on RAJAR until Q3 since it launched mid-period [Updated].

The Absolute Network suffered a small drop down 1.6% in reach and 1.3% in hours. Nothing major – but it would seem to be driven by Absolute 80s.

Finally we have the brand new Magic Network placing a strong benchmark figure of 3.7m listeners. We’ll see how it does from here on in.

Breakfast

Grimmy on Radio 1 has held his show flat this quarter, which is actually a pretty decent result when compared with the station’s overall performance. He is down 7% on the previous year however. But a solid result in the circumstances.

Over on Radio 2, Chris Evans has perhaps been temporarily distracted by Top Gear – the press certainly has (has a TV show ever had its production pored over by the press in such detail?). His radio show is down a modest 2.6% to 9.472m, but down a little less on the year. Nothing to worry about here as he now concentrates on his breakfast show.

Christian O’Connell had a great set of results last quarter, so it is perhaps not surprising that he’s slipped back this time a little. But he fell just 0.1% or by 2,000 listeners. I’m sure both Bauer and Christian will be very happy with 1.923m listeners! Listening is up too.

People are always interested in how Chris Moyles is doing. As already mentioned, Moyles featured in another heavy TV campaign during at least part of this period. He’s actually down in audience a little this quarter to 694,000 nationally. This could be a slow build for Global.

London

Before talking about any particular London station, it’s always worth carefully looking at the market overall because we have seen some odd shifts around. Arguably, this quarter is no exception, with All Radio listening up 4.5% in reach and 9.7% in hours. Year on year changes are more steady, but this is worrying as it seems unlikely that overall behavioural listening patterns are changing quite so much. As ever with RAJAR, look for long term trends rather than short term blips.

Capital has lost a few listeners this quarter, down 0.9% to 2.266m (although up on the year), however it maintains its position and number one in London in reach terms.

In hours terms, Kiss can claim to be the “most listened to” commercial music station with a 17% bump in hours on the quarter, essentially righting a massive fall in hours last quarter. It’s reach is just behind Capital’s with 2.127m. So it looks like for the foreseeable future, Capital and Kiss will be slugging it out for commercial music dominance.

Heart has bounced bank from last quarter’s awful numbers, climbing 11.4% in reach to 1.724m, although it did see a fall in hours by 9.0%.

Magic on the other hand, fell back from last quarter by 6.5% to 1.632m listeners, while its hours improved 4.7%. Perhaps it was seeing some its listeners trial some sister services? (See more on this below).

LBC had a massive bump this quarter surpassing its national performance, jumping 29% in reach in London to 1.292m, and a frankly astonishing 61.5% in hours to 14.5m hours, making it the biggest commercially listened to station in London. The jump is so large as to almost be unbelievable. However, as mentioned above, there was Brexit during this quarter, and I think it’s fair to say that this was discussed more than once on LBC…

Radio X had a modest jump this quarter with a 31.2% increase in reach to 442,000, and a 27% increase in hours to 2.5m. The percentages are good, but the numbers are low.

And BBC Radio London had a massive jump from last quarter’s dismal numbers – up 44% in reach to 510,000 and 60% in hours to 3.7m. Again, could Brexit be part of this?

Sister Stations

Absolute Radio and the BBC paved the way – in essence copying something that TV had been doing prior to that. But we continue to see sub-brands or sister services popping up. We’ve had TalkSport 2, Mellow Magic and Magic Chilled just this quarter. And of course there are decades stations and Extra/Xtra stations a-plenty. But to what extent do these services share audiences with their brethren? (Yes – I’ve done this before.)

Since I’ve been chart-free so far this quarter, here’s an incomplete look at some of these services… charted! And since it’s hard to display overlaps beyond three services in just two dimensions, I’ve limited my analysis to the three biggest services within a group. Note that these are only very roughly to scale, and they default to the period over which both or all three stations would be reported.

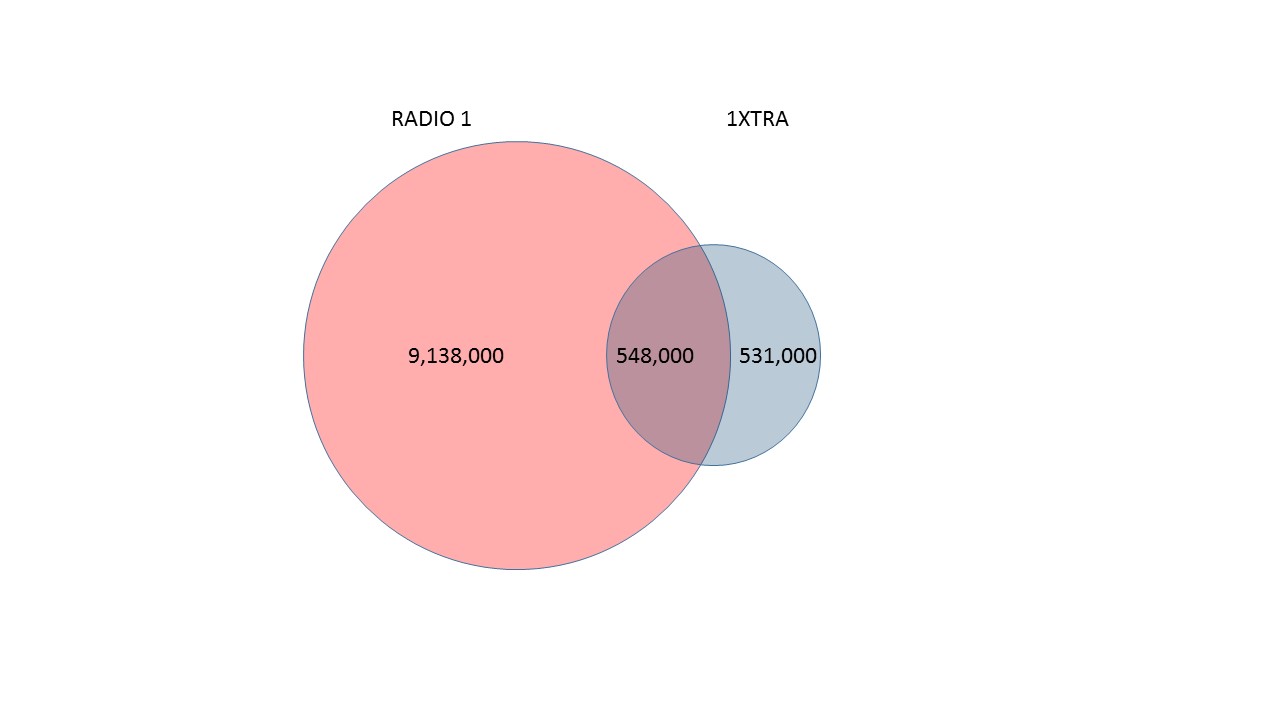

Radio 1/1Xtra

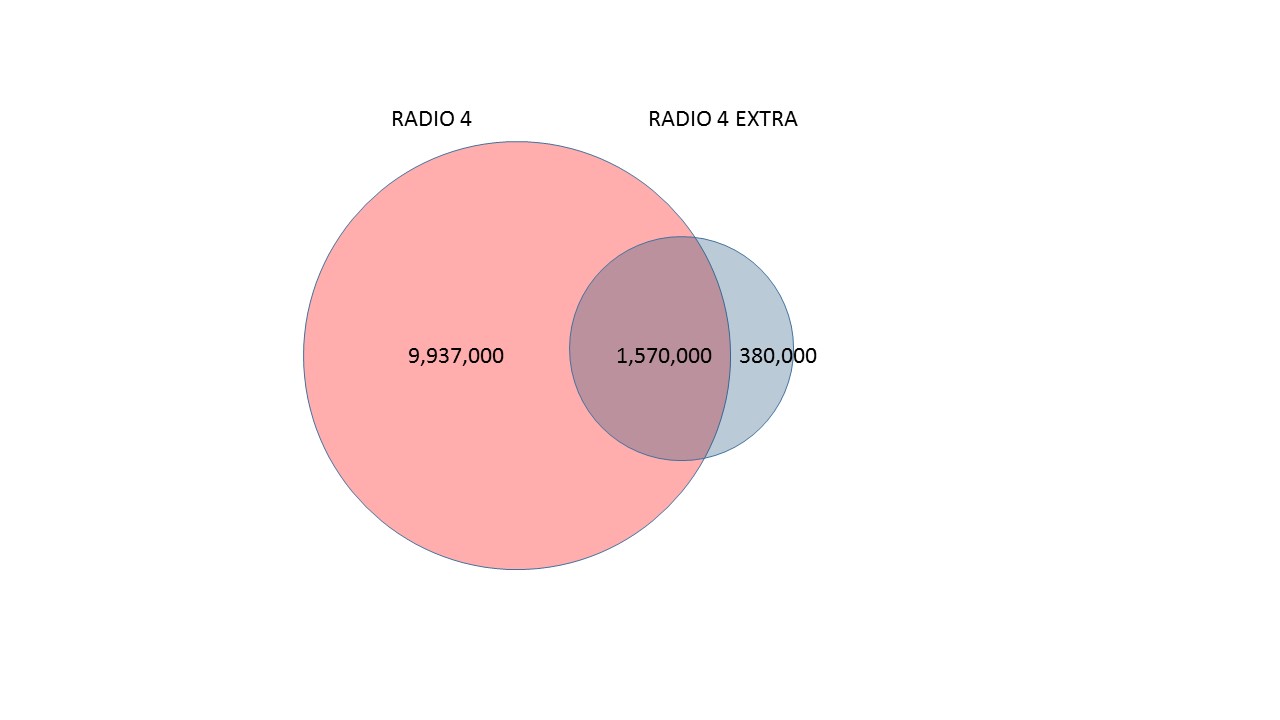

Radio 4/Radio 4 Extra

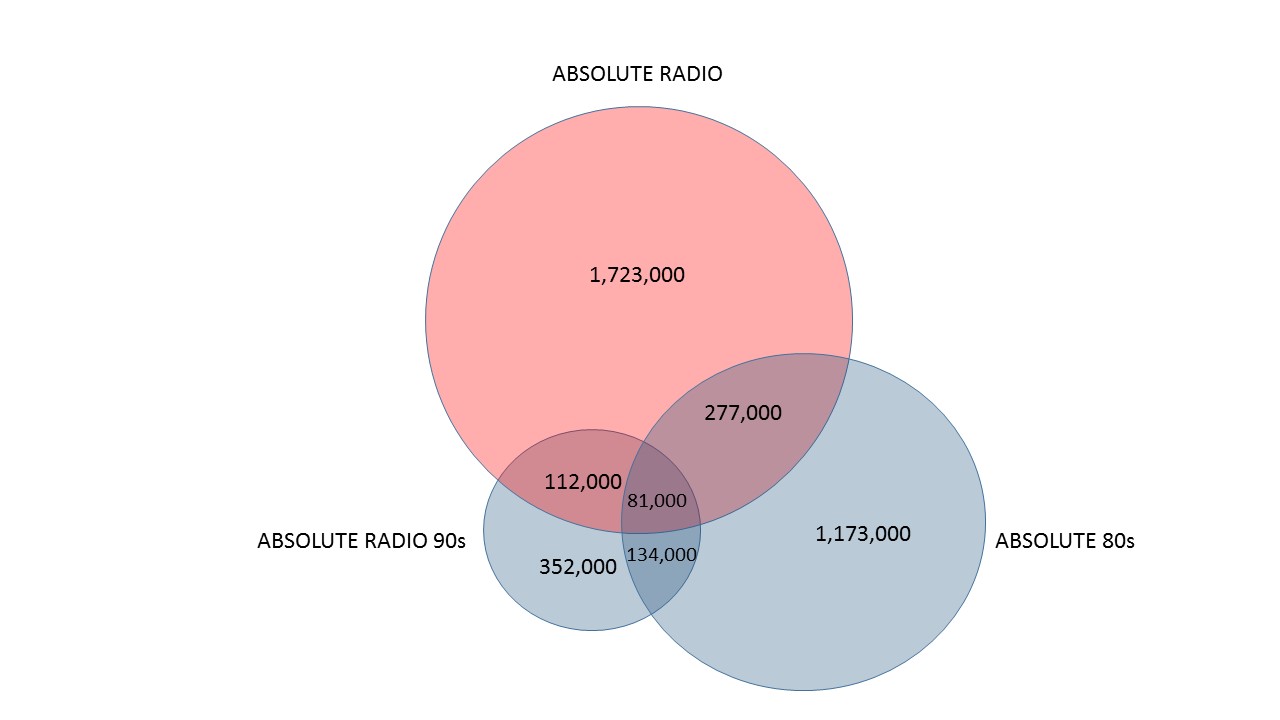

Absolute Radio/Absolute 80s/Absolute Radio 90s

Capital/Capital Xtra – London

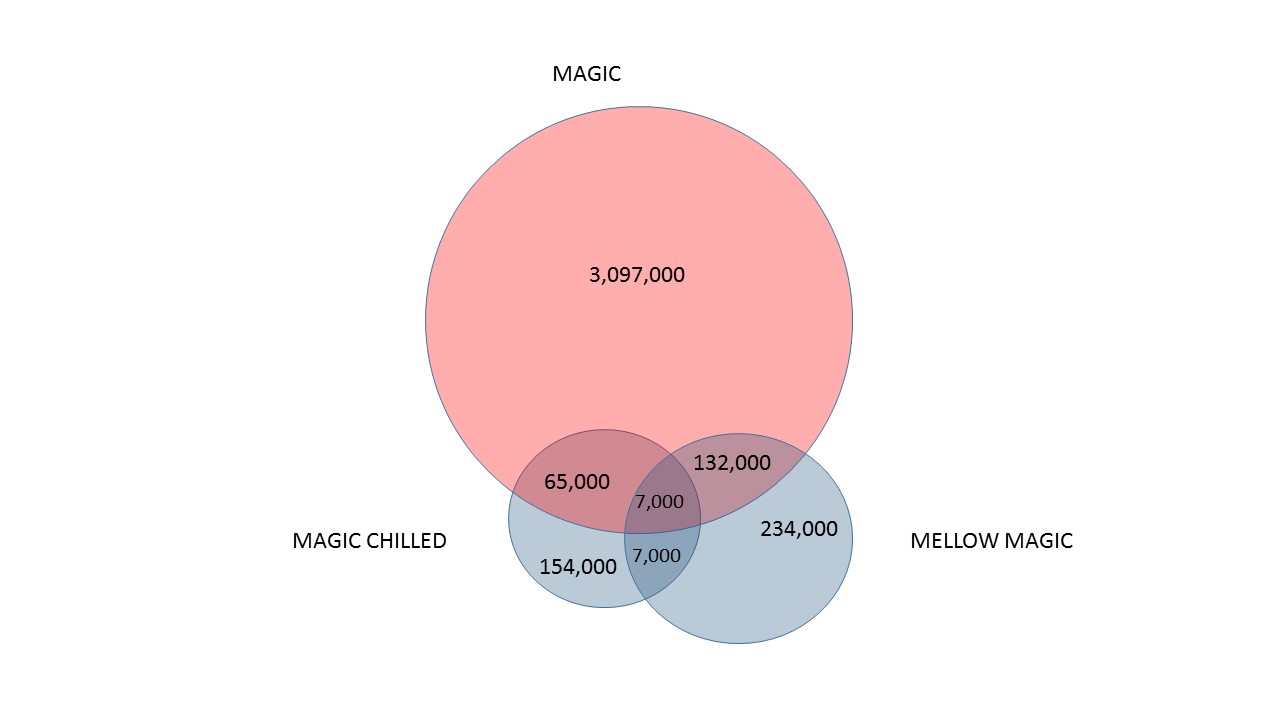

Magic/Mellow Magic/Magic Chilled

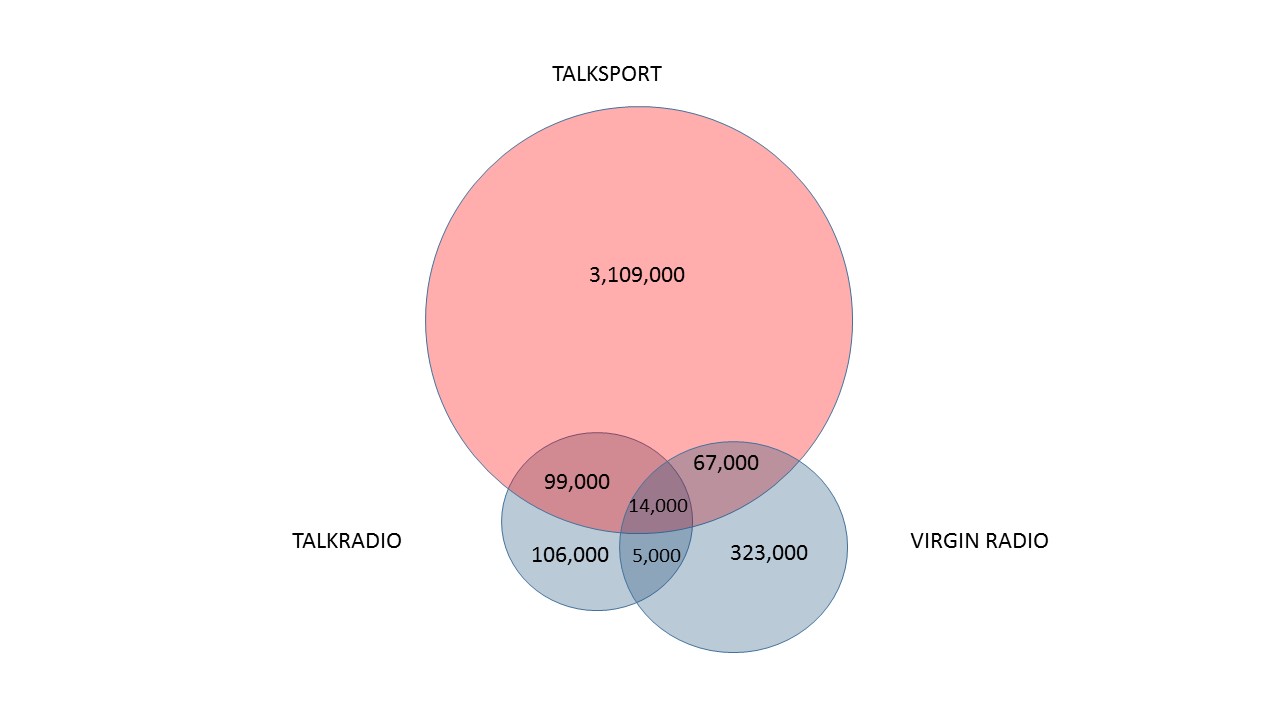

TalkSport/TalkRadio/Virgin Radio (by special request)

Further Reading

For more RAJAR analysis, I’d recommend the following sites:

The official RAJAR site and their infographic is here

Radio Today for a digest of all the main news

Go to Media.Info for lots of numbers and charts

Paul Easton for more lots analysis including London charts

Matt Deegan will have some great analysis

Media Guardian for more news and coverage

The BBC Mediacentre for BBC Radio stats and findings

Bauer Media’s corporate site.

Global Radio’s corporate site.

Source: RAJAR/Ipsos-MORI/RSMB, period ending 26 June 2016, Adults 15+.

UPDATED to correct Virgin Radio’s reach.

Disclaimer: These are my views alone and do not represent those of anyone else, including my employer. Any errors (I hope there aren’t any!) are mine alone. Drop me a note if you want clarifications on anything. Access to the RAJAR data is via RALF from DP Software as mentioned at the top of this post.

Comments

3 responses to “RAJAR Q2 2016”

Yet not a single mention for Chill

Thanks for the analysis. The Absolute and Virgin tracks overlap is distorted slightly by Absolute’s top 10 artists including The Stone Roses but Virgin’s having Stone Roses, which Compare My Radio counts differently.

Also, the proportion of unique tracks played shared by both doesn’t necessarily reflect the proportion of airtime that overlaps: if the common tracks are ones that both stations play multiple times then the on-air sound of both will seem quite similar, even if each station has a different list of more-obscure tracks that they only play once. I note that the Chilli’s ‘Dark Necessities’ is the past month’s most-played track on both stations.

Sandra Brown – Lots of stations didn’t get a mention. But if you’re a fan of Chill, it’s got to be a good thing that Global are now measuring it!

Smylers2 – You’re quite right that the Comparemyradio.com analysis is quite broad and doesn’t properly take into account the number of plays. And that’s an interesting and very valid point you make about ‘Dark Necessities.’