Once again, this post is brought to you in association with RALF from DP Software and Services. I’ve used RALF for the past 9 years, and it’s my favourite RAJAR analysis tool. So I’m delighted to be able to bring you this analysis in association with it. For more details on RALF, contact Deryck Pritchard via this link or phone 07545 425677.

Radio X

The big excitement in the radio industry this time out was to see how Radio X has done, having been re-branded from Xfm and had a huge splurge of cash spent on both new presenters and a particularly substantial marketing campaign. When Global decides to get behind something they do really get behind it.

The new station has a reach of 1.225m, up 17% on the previous quarter, and up 30% on the previous year. Both very decent figures, but I suspect that Global is looking for more.

Hours have a better story with a 43% increase on the quarter and a 49% increase on the year.

But of course the station marks a return to national radio of Chris Moyles, with much of the marketing revolving around him, including the complained about TV ad. His first book shows a reach of 671,000 up 42% on the last quarter and 41% on the last year.

The average age of the Radio X listener is 34, on a par with the final Xfm age, but perhaps a little lower than in the past.

The key thing to note about Radio X is that it’s a 6 Month weighted station. And that means that only three months’ of Radio X has been included in these numbers. So you can confidently expect the station to grow when Q1 2016’s figures are released in three months’ time.

A decent first time out, but there is still plenty of room for Radio X to grow.

Overview

Radio reach in the UK remains solidly at 90% with just over 1 billion hours of listening. But the number of hours per listener has fallen to 21.0 for the first time – people aren’t listening to quite as much radio as in the past. There are a lot of audio choices available these days.

Between the BBC and commercial radio, things are fairly even, with 53.5% of listening to BBC services, with 44.1% of listening to commercial radio.

Interestingly, commercial reach has just overtaken BBC reach for the first time, with 66% of the population listening to a commercial service against the BBC’s 65%.

Digital

It was a fairly uneventful quarter in digital terms with no growth in overall digital listening. Last quarter there had been quite a decent bump, so this was perhaps not unexpected.

The chart above shows that most platforms were basically flat this quarter. Traditionally we tend to see a bit of growth in the quarter post-Christmas when new gadgets are used for the first time. So stay tuned for Q1 2016!

Networks and Groups

6 Music has broken another all-time record, now having a reach of 2.2m (up 0.6% on the quarter and 5.7% on the year). Hours actually slipped back 1.5% this quarter so no record there, but it’s obviously a strong performer across the board.

Radio 1 saw a small fall of 2.2% on the quarter and 1.0% on the year in terms of reach. The hours story is a little worse with a fall of 7.5% on the quarter and 7.3% on the year. This again shows that while younger audiences continue to listen to the radio, they’re not listening quite as much – a challenge for everyone in radio.

Radio 2 had a modest reach increase of 0.5% on the quarter and 1.2% on the year, although hours slipped back a little to “just” 179m. Radio 2, let’s not forget, accounts for 17.5% of all radio listening in the UK more than 1 in 6 hours listened to.

I notice that the controller of Classic FM having another dig at Radio 3 in the press recently. I’m never quite sure about why that is because Classic FM has an audience of 5.5m (up 0.6% on the quarter, down 0.9% on the year) – way ahead of Radio 3’s 2.05m reach (down 0.9% on the quarter, up 1.0%) on the year. 819,000 people listen to both stations. So while a full third of Radio 3’s audience listen to Classic FM, only 15% of Classic FM’s audience ever listen to Radio 3. That suggests that Classic FM is a far bigger threat to Radio 3 than vice versa.

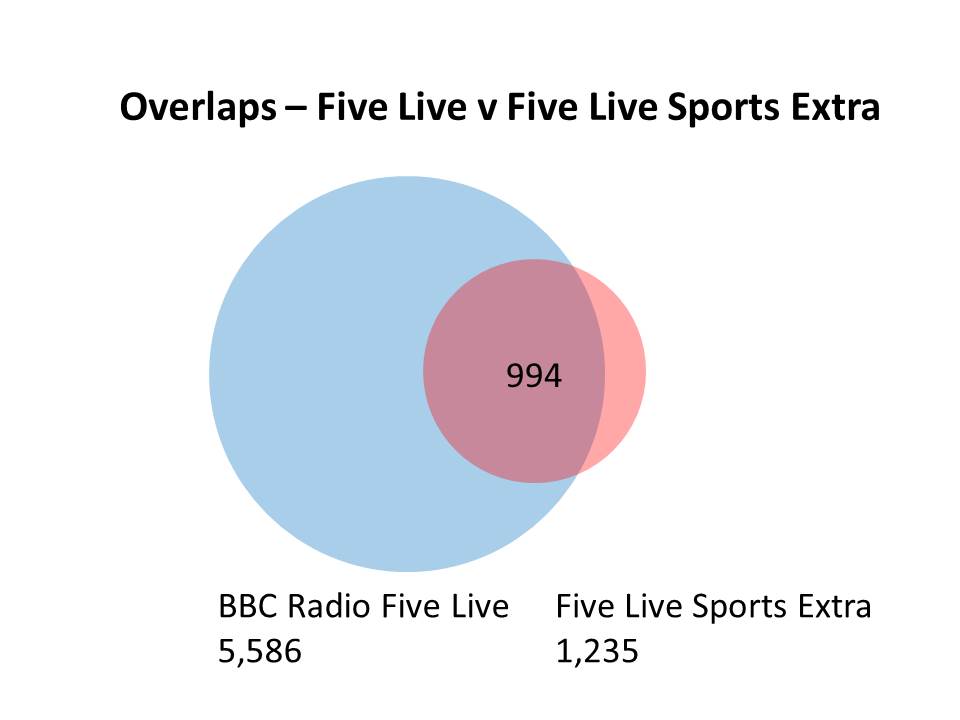

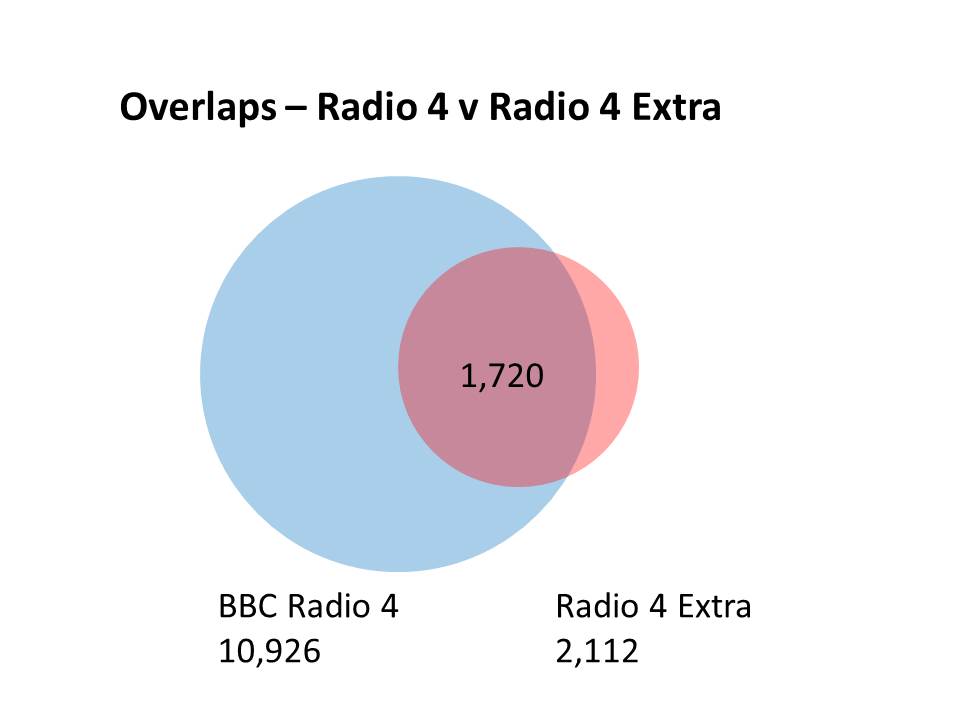

Radio 4 had a good quarter up in reach (1.4% on the quarter, 1.5% on the year) and hours (3.9% on the quarter, 4.6% on the year). And Five Live also had a good set of numbers with reach up on the quarter (1.4%) althouhg down a fraction on the year (-0.4%). Hours were stronger, now up to 11.5 hours a week – placing it as a station with one of the most loyal audiences.

Radio 4 Extra just fell behind 6 Music again in the BBC’s internal digital only battle, while Five Live Sports Extra fell back quite a lot with less compelling sport at the end of last year. Cricket in South Africa should bolster the station next quarter.

Talksport had a mixed quarter, with a reach that fell 2.9% on the quarter although up 1.9% on the year. It remains just over 3m. More concerningly, the station’s hours fell 11.8% on the quarter (down 9.4% on the year) to just over 18m. That means that the average duration for Talksport listeners is now just under 6 hours for the first time. The station will be looking to grow overall hours with the addition of Talksport 2 from next month (it launches at the Cheltenham Festival). It’ll also be interesting to hear what happens with Premier League radio rights in the coming months and whether UTV will be seeking to increase its investment to support this new service.

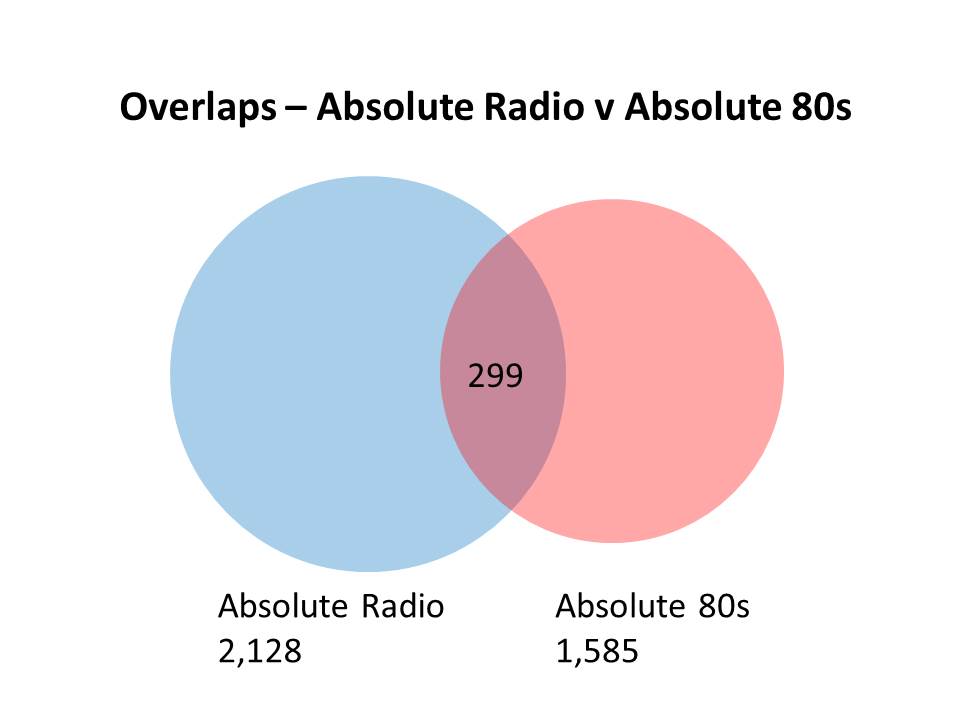

It’s been another excellent quarter for the Absolute Radio Network reaching a new record high of nearly 4.4m reach (up 4.9% on the quarter and 12.7% on the year), although hours fell a little on the quarter (down 2.9%) while still being well up on the year (12.9%).

Absolute Radio itself remains very strong, flat in reach on the quarter (0.1%) but well up on the year (24.6%) following the inclusion of the Midlands’ FM transmitter. Hours will be a little more concerning, down 10.5% on the quarter while still 24.7% up on the year.

Absolute 80s remains the biggest commercial digital only station – the closest competition being Bauer stable-mate Kisstory. The station is up 0.9% on the quarter and 11.7% on the year. Hours are even better up 7.2% on the quarter and 13.4% on the year.

The Kiss Network is flat in reach terms on the quarter, but up on the year. But the strong performer, as mentioned, is Kisstory which is up 7% on the quarter and 33% on the year in reach terms. With the upcoming changes to multiplexes for both Absolute 80s and Kisstory (see below), we could well see Kisstory overtake Absolute 80s in the future.

The Capital Network looks to have done OK, up a little in reach, and down a touch in hours, but it should be noted that the former Juice FM in Liverpool, which has just been rebranded as Capital, is included in this number.

The Heart Network is basically flat in reach terms, both on the quarter and on the year. With the upcoming sister service, it’ll be worth watching to see if the brand continues to grow.

LBC nationally had a slight fall on the quarter (down 2.8%) but is still 8% up on the year to 1.44m. There’s a similar story with hours where it’s down on the quarter but up on the year. That all said, many stations would kill for the 9.8 hours a week its average listener spends with the station (even if it was once much more than even that). It’ll be facing renewed competition from TalkRadio soon, and it’ll be interesting to see both how the two compare in the future – not just in terms of audience but also in tone.

Smooth as a network did OK, but I’m curious a little about Smooth Extra. This is only the second quarter that it has been reported and it actually fell from 930,000 to 904,000. Now for one month of that period, it was rebranded as Smooth Christmas and played only Christmas music (Clearly I didn’t listen to it). But that seems to have actually harmed rather than help its figures. But would a RAJAR diarist know that Smooth Extra and Smooth Christmas were the same service?

And finally there’s another new service this quarter – UCB 1 (formerly known as UCB) – the Christian service. Its first reach was a very creditable 236,000. Given that the service is effectively funded by its own listeners, this performance isn’t surprising. The operators obviously know that they have a substantial listenership. Whether this means that UCB 1 will be taking advertising soon is another question.

London

London is a bit of an oddity this time around, in that everyone seems to have done well. Well nearly everyone!

The issue really comes from the fact that last quarter, All Radio listening in London fell quite precipitously from 89% to 85%. This seems to have been a one-off, and listening in the capital has returned to 89% this quarter.

But that increased reach means that most of the big stations did fairly well in London.

Capital regains the commercial reach crown from Kiss, although the competition remains close at the top. Both services had very small falls in reach this quarter, -0.4% for Capital and -3.5% for Kiss. But LBC has the most commercial hours in London, in a hotly contested field with Kiss, Capital and Magic all with over 10m hours. LBC has had a quarter on quarter jump of 21% to leap ahead of the pack to 10.9m hours.

Capital has been hardest hit. While it was basically flat in reach, its hours fell 21% on the quarter (although remain flat on the year).

The rebranded BBC Radio London (formerly BBC London 94.9) saw an increase on the year (up 8.9%) although a fall on the quarter (-2.1%) as perhaps listeners learn and adapt to the new schedule.

Finally, this quarter saw a first result for The Wireless from Age UK. This is a service that has run on DAB in London for a number of years. It does report nationally since it’s available online, but a reach of 24,000 suggests that going onto RAJAR mightn’t have been advisable.

Breakfast

Nick Grimshaw saw a small increase of 0.4% on the quarter (a fall of 2.0% on the year) to 5.8m this time around.

Chris Evans saw a small dip on Radio 2 of 1.6% on the quarter and 2.0% on the year to 9.409m. While on Radio 4, the Today Programme is up 2% on the quarter and year to 6.9m.

On Absolute Radio, Christian has had a decent set of numbers. Down 2.5% on the quarter, he’s up 3.2% on the year to 1.84m at breakfast across the Absolute Radio Network.

In London, the Today Programme is the most listened to breakfast programme with nearly 2m listeners. But nobody is interested in that. They want to know about the commercial fight. Lisa Snowdon finished her final quarter on the Capital breakfast show with Dave Berry as the market leader. It was up 10.2% on the quarter and 14.8% on the year.

It’s more than 100,000 clear of the next nearest commercial service – Magic Breakfast with Nick Snaith. That show has bounced back from 771,000 last quarter to 935,000 this quarter – a 21.3% jump.

Kiss has also seen a jump, increasing 15.5% on the previous quarter (0.1% on the previous year), while Heart breakfast positively leaps 44.2% from the last quarter (a more modest 8.8% up the last year).

And on Absolute Radio, as Christian O’Connell was approaching his tenth anniversary (since passed) he was up 22% on the quarter (29% on the year) to 422,000.

All of these astounding leaps are likely to be down to some very low overall listening numbers in London last quarter as mentioned above.

The chart above shows Radio 2 and Radio 4’s performance across the day, and I think demonstrates their importance in the overall radio ecology.

If we remove All Radio, you can see that although Radio 2 is the bigger station, there are times during the day when Radio 4 is bigger.

At 8am in the morning, the stations are particularly closely matched.

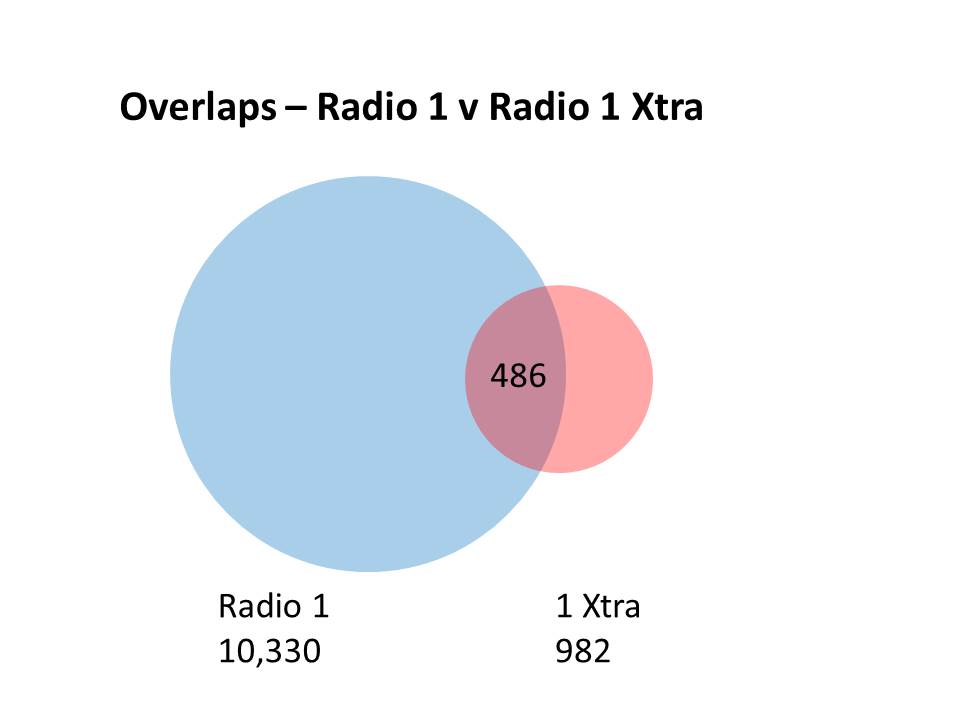

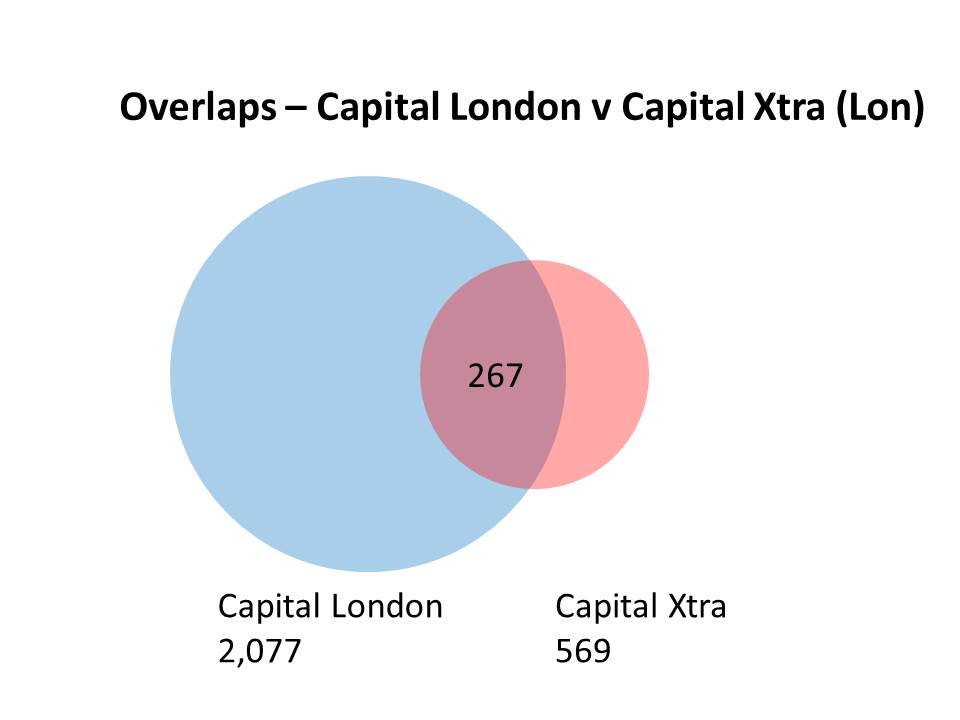

Overlaps

I did some of these a few quarters back, and I thought it was worth looking at again. Here I’ve shown the overlaps between sister stations of the same brand to show how not everyone who listens to the sub-brand listens to the main station as well.

Note that in terms of design, these are only rough approximations and not accurately sized. Also each chart is only really consistent within itself. Still you can see easily the relative sizes, and the numbers are accurate.

This is the biggest example here of a unique audience to the sub-brand who don’t listen to the main service.

D2 – The Second National Commercial Multiplex

Also just announced and worth mentioning, although not really part of RAJAR, is the full line-up for Sound Digital – the second national commercial DAB multiplex. They’re going to squeeze a massive 18 services onto one multiplex. I think it’s fair to expect that none of the regular DAB services will be in stereo (The DAB+ services will be however!).

Yes – most DAB radios are mono. But some aren’t, and a mono service just sounds worse than a stereo one. Music is, after all, made in stereo. The real place where it makes a difference is in car. Listen to Radio X and 6 Music in a car, and the difference is massive. One sounds much more enveloping that the other. Even as a listener if you don’t know why one sounds better, it will. Moan over.

For the most part, the new services launching – both here and elsewhere – are spin-offs of known brands. In due course it will be interesting to see whether audiences are pulled over from the BBC, or whether the current audience to these services will be divided up a little more. In some ways, neither matter. If new services can be delivered on a cost-effective basis, and audiences are happy with what they get, then that works well for radio groups.

A few services like Planet Rock and Absolute 80s, are shifting across to the new multiplex – leaving space for the likes of Heart Extra to launch on D1. The move to D2 will cost those services listeners however, since the geographic coverage of D2 just isn’t as good, and some people currently listening to those services on DAB will no longer be able to.

On another note it’s interesting to see a few new services not previously announced appearing on the mux.

So we have Magic Chilled (a second Magic sister service) which will be sitting alongside the also the new and now slightly renamed Mellow Magic (as opposed to the slightly odd ‘Magic Mellow’ as it was initially announced).

British Muslim Radio will now be called Awesome Radio. And as previously announced, Share Radio will be taking slot that was initially going to be used by TalkBusiness.

Finally, both Fun Kids and Jazz FM will both be appearing in DAB+ (in stereo), which is good news for both services. The big unknown is what percentage of DAB radios currently in use are DAB+ compatible. I’ll know doubt be evaluating the radios in my own home come the end of the month.

Further Reading

For more RAJAR analysis, I’d recommend the following sites:

The official RAJAR site and their infographic is here

Radio Today for a digest of all the main news

Go to Media.Info for lots of numbers and charts

Paul Easton for more analysis including London charts

Matt Deegan will have some great analysis

Media Guardian for more news and coverage

The BBC Mediacentre for BBC Radio stats and findings

Bauer Media’s site.

Global Radio’s site.

Source: RAJAR/Ipsos-MORI/RSMB, period ending 20 December 2015, Adults 15+.

Disclaimer: These are my views alone and do not represent those of anyone else, including my employer. Any errors (I hope there aren’t any!) are mine alone. Drop me a note if you want clarifications on anything. Access to the RAJAR data is via RALF from DP Software as mentioned at the top of this post.

Comments

2 responses to “RAJAR Q4 2015”

Can’t wait for LBC to face some serious competition. When are you expecting TalkRadio?

[…] my recent RAJAR post, I wrote a little about the second national commercial multiplex – Sound Digital – […]