This post is brought to you in association with RALF from DP Software and Services. I’ve used RALF for the many years, and it’s my favourite RAJAR analysis tool. So I am delighted that I continue to be able to bring you this RAJAR analysis in association with RALF. For more details on the product, contact Deryck Pritchard via this link or phone 07545 42567

Ken Bruce, Greatest Hits Radio and Radio 2

Welcome to another RAJAR release, where the biggest story today is likely to be how Ken Bruce, Greatest Hits Radio and Radio 2 have all done.

A reminder that Bruce’s final show for Radio 2 was on 3 March 2023, which fell into the Q1 2023 RAJAR period. His first show for Greatest Hits Radio was on the 3 April 2023.

The complicating factor is that Greatest Hits Radio is a 6 month station, meaning that data collected is measured across a rolling six month period. So the new numbers published today are from January 2023 all the way through until June 2023, and Bruce was only in place for 3 of those months. It’s also worth noting that Greatest Hits Radio’s owner, Bauer, has been rebranding stations in their portfolio to “Greatest Hits” over the last few months (Indeed, this is something that will continue, since Ofcom recently gave permission for Bauer to rebrand Kiss FM in the East of England to Greatest Hits Radio, which will no doubt take place soon).

Meanwhile, Radio 2 is measured quarterly, meaning an entirely fresh set of data every 3 months. And that does mean that technically, you’re not comparing the stations on a like-for-like basis.

With all of that explained, Greatest Hits Radio was up 13.1% on the quarter and up 58.9% on the year to 5.787m. Both of those increases can at least in part be explained by stations being rebranded, but the station is definitely in the ascendant, and of course they now have a new record audience. (NB. Bauer does also have Greatest Hits Radio Network which includes Downtown Country Radio. I’m just using the main Greatest Hits Radio numbers here, because the main GHR shows are not carried by Downtown Country – that’s more of a sales concern.)

Interestingly, the average age of a Greatest Hits Radio listener jumped from 49 to 51 this quarter (a year ago it was just 47). That might suggest that Bruce is bringing across some older listeners.

Bruce’s new timeslot on Greatest Hits is 1000-1300 on weekdays, as opposed to 0930-1200 when he was on Radio 2.

Bruce’s show in Q2 reached 2.991m listeners, a 37% increase over the 2.182m listeners in that slot the previous quarter, and 93% up on the same slot a year earlier.

But to put that in perspective, his final Radio 2 set of figures was 8.3m – so he has around 5.3m fewer listeners than he used to.

Of course, his Greatest Hits audience will grow, even if just by virtue of the RAJAR methodology and 6 month weighting coming into play, never mind the further rebranding of stations to Greatest Hits by Bauer, and any marketing that takes place.

And there has been significant marketing, with plenty of ads visible certainly in London where I live.

What about over on Radio 2? How has the station been impacted by the loss of Bruce?

Quite a bit, as it happens. The station is down 1m listeners on the quarter falling 6.9% on the quarter and it’s down 7.4% on the year. It now has 13.456m listeners.

While that’s still by far the biggest radio station in the UK (and quite possibly Europe), you’d have to go back to 2009 for the last time the audience was this “low”, and care should be taken making such comparisons, because the RAJAR methodology has changed over that time. What is true is that Radio 2’s audience has been remarkably consistent over recent years, as they’ve ridden out departures like Chris Evans, Simon Mayo and Graham Norton without too much audience churn.

Considering that Bruce’s mid-morning show had grown to be the biggest show on the station, it perhaps isn’t surprising that the numbers have dipped.

Perhaps of greater concern is the fall in listening hours – down 14.3% on the quarter and down 15.2% on the year to 131m (from 153m).

Vernon Kay’s new show, taking the place of Bruce’s, started on 15 May – around halfway through the quarter, with Gary Davies mostly filling in the gap between Bruce’s departure and Kay’s start. So again, that needs to be considered when looking at Kay’s numbers.

The first set of numbers for Kay show that he has 6.944m listeners, down 16.1% on Bruce’s last numbers.

I would suspect that there is a lot of trial going on for some of Bruce’s listeners. Obviously Kay’s and Bruce’s shows don’t quite overlap with one another: Kay’s starts earlier, and Bruce spends the final hour of his show up against Jeremy Vine.

Some listeners retuning their radios to Greatest Hits Radio for Ken Bruce might just leave retuned come breakfast the next day. While the afternoon presenters like Debbie Mac in London who are regionalised mightn’t be as familiar a name to former Radio 2 listeners, Simon Mayo during evening drive will be.

The other thing really to point out is that it’s not just as straightforward that a million listeners have left Radio 2 and they’ve all gone to Greatest Hits Radio. Some of the listeners from Radio 2 have gone to other stations. There’s also a healthy overlap between Radio 2 and Greatest Hits – in other words, listeners who spend time with both stations.

2.246m listeners spend time with both stations. That means 39% of Greatest Hits Radio listeners also listen to Radio 2 (although that number only represents 16% of Radio 2 listeners who also listen to Greatest Hits Radio).

Overall Trends

In general, All Radio listening was up this quarter, with 88% of the population listening to the radio each week – representing 49.473m people (up 0.2% on the quarter and up 1.0% on the year).

Hours spent listening to the radio were also up, with 1.016 billion hours a week consuming the media (up 0.7% on the quarter and up 1.8% on the year).

It was another good quarter for Commercial Radio, in part benefiting from the noise surrounding Bruce, with reach up 1.3% on the quarter, and up 8.0% on the year to 39.192m. That’s the biggest ever reach for UK commercial radio, with 70% of the population spending at least some time listening to a commercial station.

Hours were also up very strongly, reaching 553m – up 6.6% on the quarter and up 13.2% on the year. That’s comfortably another all-time record for commercial radio.

That does mean that the BBC will have seen falls. BBC Radio reach was down 1.6% on the quarter and down 3.9% on the year to 31.680m. And hours fell to 439m, down 6.0% on the quarter and down 8.5% on the year.

National Stations

While the BBC overall, and Radio 2 in particular have had tough quarters, over at Radio 1 the picture is better. Reach was up 118,000 to 7.694m (up 1.8% on the quarter and up 2.9%) on the year. Hours were down 4.1% on the quarter, but up 2.3% on the year to 47.6m.

Radio 3 was down 11.8% on the quarter and down 15.8% on the year to 1.703m, while hours also fell, down 7.6% on the quarter and down 12.5% on the year to 12.877m.

Radio 4 has had another disappointing quarter, with reach down 4.6% on the quarter and down 12.9% on the year to 8.971m. You’d have to go back to 2000 the last time it was that low. Hours were also down, falling 7.7% on the quarter and down 9.5% on the year to 104m.

I did say last quarter that a single set of numbers shouldn’t be taken in isolation, but Radio 4 has now had two poor quarters in a row, which is much more indicative.

As a network that’s reliant on speech, much of which can be listened to on demand either through BBC Sounds or via podcast players, I would note that RAJAR doesn’t truly capture that on demand listening. That’s a wider discussion for another day, but in a world where we move towards on demand and away from linear listening, that will have an effect. But I would note that across the board, this does not seem to have been a great quarter for speech radio overall.

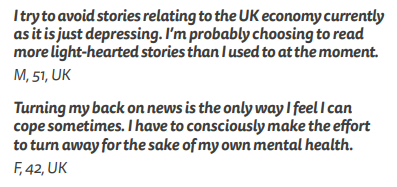

It’s probably also worth referencing some interesting figures published in the recent Reuters Digital News Report 2023. Across all the markets that the Reuters Institute report measures, active “news avoidance” has risen to around 36% of the population engaging in it at least sometimes. For the UK, that figure is higher at 41%.

A couple of illustrative quotes, lifted from page 22 of the report:

Since the UK’s speech stations are generally news-focused, I wonder to what extent whether this is a factor in some of the declines in listening that we’ve seen?

Other predominantly speech BBC radio stations have also suffered this quarter. BBC Radio 5 Live was down 1.2% on the quarter and down 1.5% on the year to 5.045m, while hours fell 1.8% on the quarter and were down 4.4% on the year to 29.857m.

And the BBC World Service was down 0.6% on the quarter, but down 23.4% on the year to 1.078m. Hours fell 14.7% on the quarter and were down 32.5% on the year to 5.026m. Regular readers may recall that there was a big fall last quarter, hence those disappointing year on year figures.

BBC 6 Music seems to have plateaued a bit recently, with reach down 1.5% on the quarter and down 6.4% on the year to 2.669m. Hours were up 4.7% on the quarter and down fractionally 0.1% on the year to 28.098m.

BBC Local Radio continues to be in the news due to planned changes, but its reach grew quarter on quarter, up 3.7% to 7.657m. Reach did fall 2.1% on the year. In terms of hours, they were up 4.1% on the quarter and up 4.1% on the year to 57.423m.

As with Radio 4 and 5 Live above, LBC (UK) was another speech casualty, with reach down 6.2% on the quarter and down 2.3% on the year to 2.549m. Hours fell very much in line with reach, down 6.4% on the quarter and down 2.1% on the year to 27.5m.

Classic FM had mixed figures with its reach down 1.5% on the quarter and down 9.9% on the year to 4.475m. Hours were up 3.6% on the quarter but down 8.9% on the year to 37.9m.

Mixed results for talkSPORT which saw its reach fall 2.3% on the quarter, but was up 19.8% on the year to 3.221m. Hours were better, up 8.0% on the quarter and up 31.5% on the year to 20.684m

At sister station TalkRadio, reach was down 13.5% on the quarter, but up 6.0% on the year to 727,000. Hours were down 19.8% on the quarter and down 10.6% on the year to 4.553m.

Times Radio saw its reach fall, down 5.6% on the quarter and down 8.2% on the year to 523,000. Hours were up however, rising 12.9% on the quarter and up 25.1% on the year to 3.945.

Not a good quarter for Virgin Radio with reach down 5.2% on the quarter and down 0.1% on the year to 1.438m. Hours were down 2.4% on the quarter and down 2.3%

Finally in this section, Boom Radio broke more records. Reach was up 0.9% on the quarter and 90.8% on the year to 641,000, while hours were up 6.8% on the quarter and 108% on the year to 6.578m.

National Brands

Aside from Greatest Hits Radio, Bauer also has its Hits Radio Network which incorporates many of its heritage FM radio brands. The number (including partners – i.e. stations it sells but doesn’t own) was down 3.2% on the quarter but up 6.8% on the year to 8.122m. Hours were better, up 1.1% on the quarter and up 2.3% on the year to 64.270m.

Kiss had saw a modest reach increase on the quarter, up 0.2%, to 2.446m (up 2.2% on the year). Hours were mixed, down 3.8% on the quarter and up 4.2% on the year to 9.973m.

Across the entire Kiss Network, reach was up 1.7% on the quarter and up 3.2% on the year to 4.244m. Hours were down 0.3% on the quarter but up 5.3% on the year to 21.038m.

But the big news in the Kiss world is that Kisstory has overtaken the main Kiss station for the first time!

Kisstory had massive growth this period, with reach up 17.5% on the quarter and 10.7% on the year to 2.544m. Hours were up 12.3% on the quarter and up 2.8% on the year to 11.064m. So Kisstory has 58,000 more listeners than Kiss (it has more hours too).

Magic saw some falls this quarter, with reach down 5.2% on the quarter and down 1.8% on the year to 2.708m. Hours fell 6.7% on the quarter and were down 5.2% on the year to 14.289m.

Overall, the entire Magic Network was down 4.2% on the quarter, but up 0.2% on the year to 3.860m. Hours were down 6.2% on the quarter and down 2.6% on the year to 21.279m.

Over at Absolute Radio, reach was down 3.0% on the quarter, but up 6.1% on the year to 2.357m. Hours were up 8.0% on the quarter and up 3.3% on the year to 16.531m.

It was a decent quarter for Absolute 80s with reach up 18.4% on the quarter and up 17.8% on the year to 1.720m. Hours were up 10.4% on the quarter and up 28.7% on the year to 8.639m. Those figures may in part explain why the station has just launched a premium Forgotten 80s sub-brand based around the long-running Matthew Rudd presented show of the same name.

Overall the Absolute Radio Network was up 1.7% on the quarter and up 7.5% on the year to 5.431m. Hours were up 10.0% on the quarter and up 11.2% on the year to 38.547m.

In a quarter that saw another edition of their very successful Summertime Balls the Capital Network (UK) saw its reach fall 2.2% on the quarter, but increase 6.1% on the year to 6.013m. Hours were up 4.1% on the quarter and up 9.1% on the year to 30.367m.

Across the entire Capital Brand (UK) reach fell 0.6% on the quarter, but was up 7.0% on the year to 7.791m, while hours rose 4.6% on the quarter and were up 10.7% on the year to 41.146m.

And there’s a new Capital branded station this quarter. Capital Chill is reporting RAJAR figures once again. Not to be confused (as I initially was) with Smooth Radio Chill (or Magic Chilled for that matter) which was the original Chill, this is a new service with 178,000 listeners and 792,000 hours. This does feel like a response to people using their smart speakers to play “chillout music” or similar.

Another completely new radio station reporting this quarter is Radio X Classic Rock, which has launched with 275,000 reach and 1.360m hours. That’s a pretty decent first quarter for a digital-only brand.

Overall the Radio X Network was down 1.9% on the quarter and up 4.1% on the year to 1.975m reach. Hours were down 0.3% on the quarter and down 12.4% on the year to 16.421m. (There is a new Radio X Brand incorporating the new service which brings the overall figures up to 2.097m reach and 17.142m hours).

The Smooth Radio Network (UK) is down 2.1% on the quarter and up 9.0% on the year to 5.141m. Hours were up 4.2% on the quarter and up 9.7% on the year to 36.073m. Across the entire Smooth Radio Brand reach was down a tiny 0.1% on the quarter and up 7.9% on the year to 5.878m. Hours were up 4.8% on the quarter and up 11.0% on the year to 41.323m.

Generally good results for the Heart Brand (UK) with reach down 1.0% on the quarter but up 14.5% on the year to 11.140m. Hours were up 3.2% on the quarter and up 20.1% on the year to 75.575m – the biggest brand sale available in UK commercial radio.

Across the Heart Network (UK) reach was down 4.2% on the quarter but up 9.7% on the year to 8.520m. Hours were down 2.1% on the quarter and up 8.5% on the year to 55.420m.

In the ongoing battle of the 80s stations, Heart 80s continues to lag just being Absolute 80s. Reach was up 1.0% on the quarter and up 19.8% on the year to 1.587m. Hours were also good, up 1.7% on the quarter and up 25.3% on the year to 6.171m.

Note: There was no MIDAS data this quarter. Look out for that with the next RAJAR release in October.

Further Reading and Listening

I will once again be discussing all things RAJAR with Matt Deegan on The Media Podcast, which will be coming a day early on Thursday. Listen wherever you get your podcasts!

Matt Deegan himself will also be writing about RAJAR on his blog and email newsletter. You should sign up if you haven’t already.

The official RAJAR site has all the topline figures

Radio Today for a digest of all the main news

Media.Info for lots of numbers and charts

The Media Leader will have analysis

BBC Mediacentre for BBC Radio stats and findings

Bauer Media’s corporate site

Global Radio’s corporate site

Radiocentre’s website

All my previous RAJAR analyses are here.

Note: Updated details on regionalised afternoon show on GHR. Also corrected details about Capital Chill not being the same station as the original Chill.

Source: RAJAR/Ipsos MORI/RSMB, period ending 25 June 2023, Adults 15+.

Disclaimer: These are my views alone and do not represent those of anyone else, including my employer. Any errors (I hope there aren’t any!) are mine alone. Drop me a note if you want clarifications on anything. Access to the RAJAR data is via RALF from DP Software as mentioned at the top of this post.

Comments

4 responses to “RAJAR Q2 2023”

Just a small correction – GHR breakfast isn’t regionalised, there are just 2 versions – Scotland and everywhere else. The afternoon show, which you mention as being Debbie Mac, is the regionalised slot.

Isn’t Smooth Chill a continuation of the former Chill service, with Capital Chill a new, separate service? Not sure, just wondering if I’ve got that muddled up somewhere.

@Chris – Thanks for that. I’ll amend accordingly!

@Abigail – You are quite right. I’m getting my Chills confused! This is indeed a completely new one to RAJAR.